After 28 years as a Practising Member of the REIQ, this Fellow Membership arrived today 😊Humbled and grateful, for the recognition of a journey that spans over three decades. Receiving the Fellow Membership at the REIQ is not just an honor; it’s a testament to the enduring belief that patience and perseverance, word of mouth referrals, and being hard at work each and every day for our Clients, tenants and maintenance people.

36 years ago, I embarked on a path that many saw as a changing the world and helping people, a dreamer’s pursuit. Yet, here we are, celebrating a milestone that speaks as much to our loyal Clients support and encouragement as it does to my steadfast commitment, inclusive of Carlos, Paula and Hazel ❤️

BBest Regards.

Linda-Jane姬琳达珍 Debello FREIQ, LREA, LJ Gilland Real Estate Property Sales & Management Est 1996

Latest Five Star Landlord & Vendor Rate My Agent Reviews ***** Excellent Service *****

*****5 Stars*****

Excellent all round

I have used LJ Gilland Real Estate for well over a decade managing my rental property. In that time they have earned my respect as a trustable, honest and forthright team. It was an easy decision to turn to Linda and Carlos to sell my property. Their approach was devoid of the jargon and spin other real estate agents deal in. The outcome was great for both myself and the new owner. A quick sale for a good price. I highly recommend the LJ Gilland team.

Review submitted by Jason Pont (Vendor) on 30 Jan 2024

Listed on Thursday, Open House Saturday, sold on Tuesday — need we say more!!! We would like to express our heartfelt appreciation for the exceptional service provided by Carlos and Linda from LJ Gilland Real Estate during the recent sale of our property. Your professionalism, dedication and expertise truly made a significant difference in our home selling experience. From the very beginning, you demonstrated an in depth understanding of the local property market and this proved invaluable in securing the sale of our property. Throughout the process, your communication and responsiveness were exemplary and your patience in answering all our questions demonstrated your commitment to ensuring a successful sale. Your negotiation skills were impressive, as was your attention to detail particularly in organising some minor maintenance tasks that needed to be completed prior to settlement. In a competitive Real Estate market your friendly and approachable demeanour made working with you a pleasure. We wholeheartedly recommend your Real Estate services to anyone looking to buy, sell or rent. Thank you again Carlos, Linda and all of the staff at LJ Gilland Real Estate. Kind regards Wayne and Sandra Warren Review submitted by Sandra & Wayne Warren (Vendor) on 25 Oct 2023

Post a review to our Google Business profile as this is another portal for which we help spread the word and promote rental and sale listings to help our Clients i.e. https://g.page/ljgrealestate/review?gm

The information in this message is intended for the recipient named on this email. If you are not that recipient, please do not read, copy, distribute or act upon the message as the information it contains may be privileged and confidential. If you have received this message in error, please notify us immediately by return email. Thank you for your co-operation P Please consider the environment before printing this email

Linda and her team have managed our investment property from Day 1. They have been totally organized, prompt and responsive to any requests during the rental period. Excellent vetting of tenants, with proactive management of the property. 12 months ago we were ready to sell, however Linda’s guidance and advice suggested we should wait – which we did. Recently we decided to sell – that advice gained us an additional, yes additional, 60% over what we would have achieved previously. Very happy with her professionalism, knowledge & guidance.

⭐️⭐️⭐️⭐️⭐️

Carlos and I are very appreciative and thankful for your kind words. As a team, LJ Gilland Real Estate were privileged to look after your Investment Property, treating it as if it was our own. Please stay in touch with us for many more years as our relationship is more than just the long term business, it’s a loyal trusting friendship. Thank you.

Carlos and his wife were very helpful. I bombarded them with lots of questions and they had excellent knowledge of the property we were interested in. I am sure I was quite a complicated client. I had no experience in buying a property. Carlos is a great communicator, kept in regular touch by phone or internet, and guided me through. We are very happy with the property and the process. Thank you !!

#testimonials #property-investors #valued #landlords #referrals over 22 years #word-of-mouth #family #realestate

Rental house property management and sale.

Vendor Review – Recommended by HowardJeanelyTatters

15 Feb 2017

Ten years we had our rental property, L.J Gilland managed it, in all that time we never had a bad renter in our house because the applicants were carefully chosen. When it came time to sell, we had L J Gilland to handle the sale, they did low cost advertising because they have a large data base of investors who they contacted about our house which gave us a quick sale and at a price we were very happy with.

No hassle agency

Buyer Review – Recommended by AbidRasheed

22 Feb 2017

Very responsive, prompt and easy to deal with. Don’t try try to overdo things and quite

• Property management & Sales of Tenanted Investment Properties is our Speciality – Core Business.

• Individual solutions to fit our client’s needs

• Body corporate management

• Competitive Commission Rates

• LET FEE FOR REFERRALS, We are a business built on over 30 years of Referrals.

• NO Lease Renewal & Comparable Market Analysis’ Fees/Charges

• PHOTOS TAKEN ON ENTRY, tenants are shown about safety switches and water mains etc. We meet all tenants on site.

• Hands on approach to all Property Investment Management Matters.

Dedicated to implementing best practice, achieving set goals and encompassing a consistent approach to quality management and making effective use of all available technology. We recognize that tenants are customers too, treating them with any sort of disrespect would be detrimental to all property investor’s. It is all about Attitude. We Aim to remove the hassle from Sales & Rentals

Linda is a dedicated and honest real estate agent with a high level of attention to detail. Linda helped me throughout the way with the whole buying process. She followed up on her promises and assisted in ensuring the buying process was problem free. She has a significant level of industry experience and would recommend her to anyone for the sale and purchase of a property.

******** DUE TO COVID – TO VIEW THIS MAGNIFICENT MANSFIELD HOME ALL BUYERS MUST BE REGISTERED TO ATTEND OPEN HOME BY EMAILING AGENT – ADMIN@LJGREALESTATE.COM.AU – ACCESS WILL NOT BE GRANTED FOR UNREGISTERED ATTENDEES ********

This elevated family solid brick home boasting spectacular views has 3 generous sized bedrooms, main with air-conditioning, all with built-in cupboards, separate toilet and bathroom upstairs with a second toilet and shower downstairs.

This property boasts spacious living and dining with sliding doors leading onto a front veranda where you can relax and enjoy afternoon breezes while taking in the expansive view. From the moment you arrive, you will be charmed by the traditional colour schemes and solid brick facade, and stepping inside these classic features continue with the generously sized airconditioned dining and living area synonymous with homes of this era.

A unique feature of this home is the wonderful sunroom on the main house level.

At a Glance:- • 2-Storey Solid Brick Home with Spectacular Views • 3 Good Sized Bedrooms (main with air-con) • Bathroom and Separate Toilet Upstairs • Authentic Large 70’s styled kitchen • Airconditioned Dining/Lounge with Sliding doors leading to Tiled Front Veranda • Massive Sunroom • Chandeliers • Internal Laundry leading off the kitchen area • Downstairs toilet, shower, office/workshop • Massive amount of storage • Double Garage • Block size 650 sqm • Close to all amenities

Rates $490.55 p/qtr For those who need storage space, you will be pleased to know that downstairs includes a large 2 car garage plus an additional storage area and study/workshop.

Perfectly positioned within the coveted Mansfield State High and Primary School catchment zone, and just a stone’s throw from Brisbane Adventist College, this elevated brick home is sure to impress. A number of other state and private schools are within easy reach including Brisbane Adventist College, Wishart State School, St Catherine’s Primary School, and Citipointe College. Only the second time on the market in its lifetime as this property has been tightly held by the current owner for over 47 years.

This property is sure to generate a significant amount of attention and will be sold quickly, so be quick not to miss this opportunity to secure a perfect family home positioned in the Mansfield school catchment and within easy walking distance to all amenities. Aminya Street shops at the end of the street boast a Medical Centre, Pharmacy, Dentist, Post Office, Grocery Store, Bakery, Café, Sam’s Pizza and more.

Just a short drive to Westfield Carindale & Westfield Garden City and only a few metres to Express buses to the City and Westfield Garden City. Everything is so close or easily accessed by public transport that you could leave the car in the garage.

The information in this message is intended for the recipient named on this email. If you are not that recipient, please do not read, copy, distribute or act upon the message as the information it contains may be privileged and confidential. If you have received this message in error, please notify us immediately by return email. Thank you for your co-operation

Please consider the environment before printing this email

The rate of property price decline continues to ease-Overall we are seeing further evidence that the worst of the housing market conditions might now be behind us. Hear all the national and state based insights here.

In this month’s housing marketing update, CoreLogic share that Australian dwelling values fell half a percent last month as the pace of home value declines continued to ease after moving through a recent low point in December last year when national dwelling values were falling at a much faster rate. The latest figures take national housing values 7.2% lower over the past twelve months to be down 7.9% since peaking in September 2017.

The slowing of the rate of decline is attributable to an easing in the market downturn across Sydney and Melbourne where an improving trend in the rate of decline has been evident over the past three months. In December last year, Sydney dwelling values were down -1.8%, with the pace of falls progressively moderating back to a month on month decline of 0.7% in April. Similarly, Melbourne values were down -1.5% in December, with the rate of decline slowing to -0.6% in April.

Although the national rate of decline has improved, the geographical scope of falling values has broadened. In April, dwelling values fell across every capital city apart from Canberra, while regional areas of Tasmania, Victoria and South Australia also avoided a fall. The broad-based nature of weak housing market conditions highlights that tighter credit conditions are having a dampening effect across all markets.

Annually, national dwelling values were down -7.2%; the largest decline since the twelve months ending February 2009, which was associated with the Global Financial Crisis.

Overall we are seeing further evidence that the worst of the housing market conditions might now be behind us. Values are still broadly declining, however the pace of decline has moderated since December last year and there are some tentative signs that credit flows have improved, albeit from a low base.

Considering that tighter credit conditions were one of the primary catalysts for the housing market downturn, any sign that credit availability is improving would be a welcome outcome for the housing market.

According to the Australian Bureau of Statistics, lending to households for dwellings, excluding refinancing was up 2.7% on a seasonally adjusted basis in February. Additionally, a rise in CoreLogic valuation platform activity throughout March hints at a further improvement in housing finance, which will likely be reported in the next ABS release.

Another indicator of a subtle improvement in the housing market can be seen in auction clearance rates that are holding around the mid-to-low 50% range, albeit on low volumes relative to a year ago. The correlation between auction results and housing market conditions is strongest in Melbourne and Sydney where auctions comprise a larger proportion of selling activity.

While a mid-50% clearance rate doesn’t suggest housing prices are set to bounce back, it does imply a closer fit between buyer and seller expectations and the improved auction success rate supports the reduced rate of decline in housing values across Sydney and Melbourne.

CoreLogic has released its first Quarterly Rental Review for 2019, showing rents have risen by 1 per cent during the first three months of this year.

Sydney is the most expensive capital city to rent with a median weekly rent of $582 per week, while Perth is the cheapest at $385.

Quarterly rents have increased across all capital cities, bar Darwin and Sydney.

The first CoreLogic Quarterly Rental Review for 2019, which tracks median rents and rental yields across Australia, shows that national weekly rents have risen by 1 per cent during the first three months of the year.

“This seasonally strong first quarter has delivered the highest increase in weekly rents since the corresponding first quarter a year ago”, says Cameron Kusher, Research Analyst for CoreLogic. “Our regional housing markets are performing marginally better than the capital cities, many of which have been experiencing weaker rental market conditions in recent years due to excess housing supply and growing investor activity.”

“Quarterly rents have increased across all capital cities, bar Sydney and Darwin. Hobart is experiencing notable growth, with rents increasing by 3.6 per cent over the past quarter. However, with a median rent of $582 per week, Sydney remains Australia’s most expensive city for tenants by far.”

The Quarterly Rental Review also highlights a national increase in yields over the past three and 12 months. Gross rental yields for the first quarter are 4.10 per cent compared to 3.95 per cent in the previous quarter and 3.77 per cent a year ago. Darwin has the highest rental yield across the country with an annual median of 6 per cent.

Key findings – rents and yields

Nationally, rents increased by +1 per cent over the March quarter and by 0.4 per cent over the past 12 months. Combined capital city rents were 0.9 per cent higher than the December 2018 quarter but -0.1 per cent lower than the previous March quarter. This is the lowest annual change since CoreLogic started tracking rents in 2005. Regional rents were slightly stronger, with a 1.1 per cent increase over the quarter and a 1.8 per cent increase over the past year.

In the first quarter, rents climbed in all capital cities except for Darwin (-0.3 per cent). Hobart was by far the strongest performer, with a 3.6 per cent increase in rent over the past quarter, followed by Perth (+1.8 per cent) and Canberra (+1.5 per cent). Hobart also experienced the highest increase in rent over the past 12 months (+5.4 per cent) while at the other end of the scale the media rent in Darwin fell by -5.7 per cent.

Nationally, the median rent is $436 per week. The median rent across the capital cities is $465 per week, and $378 per week across the regionals.

Gross rental yields have increased from 3.8 per cent to 4.1 per cent nationally. Across the combined capitals, the average rental yield is 3.8 per cent (up from 3.5 per cent). Regional yields are far higher at 5.1 per cent, up from 4.9 per cent 12 months ago.

Key findings – capital cities

Sydney remains Australia’s most expensive capital city market, with a median weekly rent of $582, despite a decline of -3.1 per cent over the past 12 months. While rents in Sydney remained the same as the previous month, they increased by 0.5 per cent over the past quarter. Sydney also has the lowest rental yields out of all capital cities, at 3.5 per cent over the past quarter.

Canberra reports a median rental cost of $550 per week, an increase of 1.5 per cent over the past quarter and 3.6 per cent over the past 12 months. Canberra is one of only two capital cities (alongside Darwin) to experience a drop in weekly rent over the past month (-0.1 per cent).

In Melbourne, rents are $454 a week – an increase of 1 per cent over the quarter and 2.1 per cent over the past 12 months. Melbourne also reported the greatest increase in rental yields out of all capital cities, with current rental yields being 3.6 per cent, compared to 3.1 per cent a year ago. Despite the rise in yields, Melbourne has the second lowest weekly rental yield out of all capital cities (after Sydney).

Brisbane rents are starting to climb again, with Brisbane now having a median weekly rent of $436.This is an increase of 0.8 per cent over the past quarter, and 1.4 per cent over the past 12 months.

Perth is the most affordable capital city to rent in with a median weekly rent of $385. However, it is showing signs of growth, achieving the second highest quarterly rate (after Hobart) with an increase of 1.8 per cent over the past 3 months. Over the past year, Perth rents have increased by 2.1 per cent.

Adelaide closely follows Perth to become the second most affordable capital city to rent a property in, with a median weekly rent of $386. Like Brisbane, it experienced a 0.8 per cent rise in rents over the March quarter. Over the past 12 months, rents in Adelaide have risen by 1.2 per cent. Gross rental yields have remained static over the year at 4.4 per cent.

Hobart reported the strongest growth in rents, up 3.6 per cent over the past quarter to $453 per week. Over the past year, rents have increased by 5.4 per cent. Hobart also reports the strongest growth over the past month, with a 1.6 per cent increase in weekly rent. Hobart also reported the second highest rental yield (after Darwin) of 5.1 per cent, which remained the same as 12 months ago.

Darwin has experienced the most significant decline in rent to achieve a median weekly rent of $458. This is down -0.3 per cent over the quarter and -5.7 per cent over the past year. In addition, Darwin also reports a drop of 0.2 per cent over the past month. However, at 6 per cent, Darwin has the highest gross rental yield out of all the capital cities (up 0.1 per cent on the past 12 months).

CoreLogic Research Analyst Cameron Kusher said the first quarter of 2019 had delivered the highest increase in weekly rents since the corresponding first quarter a year ago

“Our regional housing markets are performing marginally better than the capital cities, many of which have been experiencing weaker rental market conditions in recent years due to excess housing supply and growing investor activity,” he said.

“Quarterly rents have increased across all capital cities, bar Sydney and Darwin.

“However, with a median rent of $582 per week, Sydney remains Australia’s most expensive city for tenants by far.”

The Quarterly Rental Review also highlights a national increase in yields over the past three and 12 months.

Gross rental yields for the first quarter are 4.10 per cent compared to 3.95 per cent in the previous quarter and 3.77 per cent a year ago. Darwin has the highest rental yield across the country with an annual median of 6 per cent.

According to the ABS, total household assets were recorded at a value of $12.6 trillion at the end of 2018. Total household assets have fallen in value over both the September and December 2018 quarters taking household wealth -1.6% lower relative to June 2018. While the value of household assets have fallen by -1.6% over the past two quarters, liabilities have increased by 1.5% over the same period to reach $2.4 trillion. As a result of falling assets and rising liabilities, household net worth was recorded at $10.2 trillion, the lowest it has been since September 2017.

Based on this data from the ABS, the Reserve Bank (RBA) calculates a number of household finance ratios.

The first metric detailed from the RBA are the ratios of household and housing debt to disposable income. As at December 2018, household debt was 189.6% of disposable income, a record high and up from 188.7% the previous quarter. Housing debt was also a record high 140.2% of disposable income and had risen from 139.5% the previous quarter.

While debt levels are quite high, the ratios of asset value to disposable income are much higher. While that may be the case, it is important to understand that if asset values fall, the value of the debt typically doesn’t reduce at the same speed, which can lead to asset value erosion. As at December 2018, household assets were 927.9% of disposable incomes. This ratio has declined as property values have fallen, down from a peak of 962.1% in December 2017. Similarly the ratio of housing assets to disposable income is currently 495.3%, down from its peak of 529.7% in December 2017. The 495.3% figure is the lowest it has been since September 2016.

As a result of a reduction in the ratio of assets to disposable income, the ratio of debt to assets is climbing. Total household debt is now 20.4% of household assets, the highest it has been since March 2016. Total housing debt is 28.3% of total housing assets, the highest it has been since September 2014. Again, this reflects the fact that asset values are falling as debt increases.

Despite generational low official interest rates, the measures of interest payments to disposable income have risen over recent quarters. This is likely reflective of lenders lifting interest rates independently of any adjustment to the cash rate by the RBA. Household interest payments represented 9.1% of household disposable income in December 2018, their highest share since September 2013. Housing interest payments accounted for 7.6% of household disposable income in December 2018, their highest share since March 2013. Despite the cash rate tracking at generational lows, households are paying a proportionally higher share of interest than they have in many years.

With housing values falling and expected to keep falling, the ratio of assets to disposable incomes is likely to fall over the coming quarters. Although most households will likely remain in a position whereby the value of their assets is significantly higher than their debt, no doubt an increasing number of recent property purchasers will have higher levels of debt than the value of their asset. This is probably an area of most concern for the RBA. If this leads to reduced consumer expenditure an in-turn slower economic growth it may be a trigger for either lower official interest rates or changes to mortgage lending policies (or both). Furthermore, with household debt at record highs and households dedicating more of their income to servicing their debt at a time when interest rates are so low if household debt levels haven’t declined by the time interest rates rise it could create more challenges for households.

This data will be very important to focus on over the coming quarters.

Linda and Carlos Proudly present 12 Page Street, North Lakes. 4 bedroom 2 bathroom 2LU. #property #management since #brand #new #1999 Near New Curtains and Carpets #Freshwater Stage #School #Catchment #Westfield #Costco #Bunnings #parks #local #amenities $370 per week #available 18th April Call 07 3263 6085 to Inspect. Located in the Freshwater Estate of North Lakes and easy walk to Lake Eden and Westfield’s shopping centre in the heart of North Lakes this Cozy 4 bedroom property features:

Open Planed kitchen/ dining and family area with ceiling fans and access to the backyard.

4 Carpeted bedrooms with built-ins and ceiling fans.

Pet-friendly properties will appeal to more tenants and can achieve higher rents, but there’s more to consider than just the rental return.

Choose the right property and features – An apartment with a large outdoor area or a house with a big backyard will appeal more to pet owners. Durable flooring such as tiles is less likely to be damaged than polished floorboards or carpets.

Have a pet renting policy–Stipulate the number of pets allowed, acceptable animals or breeds, and any size limits.

Ask for a pet resume – Tenant are often happy to supply references from previous landlords or property managers. You may also wish to meet the pet beforehand.

Investigate strata bylaws – Some complexes may not allow animals, while others have rules about the type or size of pet and may require residents to register pets or ask for permission first.

Check your landlord insurance–Tenants are generally liable for damage caused by pets, apart from reasonable wear and tear, but it’s wise to check your insurance policy as well to find out exactly what is and isn’t covered.

Claim repairs at tax time–The cost of repairing reasonable wear and tear, such as refinishing floors and repainting walls, can be deducted from your rental income to minimise your tax bill.

Landlords who allow pets could boost their rental return by up to 30 per cent

Investors are always looking for ways to increase their rental return, but there’s one strategy that can boost rents by up to 30 per cent and it doesn’t involve renovating.

In almost every capital city, median asking rents for pet-friendly apartments are higher than for homes that don’t allow pets, according to Domain Group data.That means landlords who allow pets could boost their rental return by simply checking a box.

Apartments advertised as pet-friendly are rarest in Melbourne, representing less than 3 per cent of all rentals, followed by Adelaide (6 per cent) and Sydney and Canberra (both 7 per cent).

Houses are more likely to be pet-friendly, but the proportion is still low in Melbourne (9 per cent) and Sydney (21 per cent). On the other hand, more than half of Greater Brisbane rental houses allow pets, while in Darwin, more than two-thirds are pet-friendly.

Sydney investors have the most to gain by allowing pets, according to the analysis of rental listings from the March 2019 quarter. Asking rents for apartments that allow pets are 11 per cent higher than those that don’t, which equates to $60 each week or $3120 per year.

With landlords in Sydney facing tougher competition as therising supply of rental properties pushes down rents, allowing pets could provide investors with a point of difference and minimise the time a property remains on the rental market.

Sydney property manager and Property North Agency director Ben Benny said he always encouraged landlords to consider allowing pets to improve returns.

“We definitely see an increase in rents when properties are pet-friendly,” he said. “Hands down it’s the biggest inquiry we get for any property.”

In Melbourne and Darwin, rents for pet-friendly units are 8 per cent higher, and in Adelaide and Brisbane there’s a 5 per cent difference in price.

Premium highest for rare rentals

In areas where pet-friendly rentals are least common, the premium is often higher.

Less than 3 per cent of apartments in Sydney’s Canterbury-Bankstown area were advertised as pet friendly, but rents were 26 per cent higher, with landlords pocketing an extra $105 per week or $5460 per year.

In the Liverpool and Fairfield areas, only one per cent of apartments are pet-friendly, and are advertised for 18 per cent more, costing tenants an extra $60 each week or $3120 per year.

It’s a similar situation in Melbourne’s inner city, where less than one per cent of units allow pets and rents are 30 per cent higher. That trend continues among apartments in the inner east, northern suburbs and bayside areas.

Although few rentals in Melbourne were advertised as pet-friendly, Lucas Real Estate senior property manager Emma Racky said this was relatively normal, and pets were often allowed on a case-by-case basis.

“People won’t be deterred from applying just because it doesn’t specifically say it’s pet-friendly,” she said. “It just depends on the owner’s preference. Some aren’t too fussed, but if it’s a new property, they’re worried about damage.”

Restrictive landlords limit their tenant pool

In Brisbane, where pet-friendly rentals are much more common because tenants considered them part of the family.

In Brisbane, you reduce the pool of tenants if you say it’s not pet-friendly.

I love to give out a property which is pet-friendly because I know I’ll have a bigger pool of people coming through and the take-up is much faster.” In Sydney, the northern beaches has one of the highest concentrations of pet-friendly houses. More than one-third of rental houses are pet-friendly, and landlords who allow pets can expect rents to be 17 per cent higher.

Pet ownership is common among families renting houses there as trends were changing.

Over the past two or three years we’ve seen more of a shift towards younger couples, finding it more common for two-bedroom apartments.

Although property damage is a concern for many landlords, it was not the only issue. For strata buildings and apartments, the biggest concern is noise and upsetting other neighbors.

One of the biggest questions asked by property owners looking to rent out their property is whether or not to allow tenants to have pets and what the potential impact is of this decision.

NO PETS

Allowing no pets at all will potentially reduce the pool of tenants who will want to rent your property.

On the upside though, having no pets obviously means there will be less wear and tear on the property in terms of damage to the property and potentially, odours in the property.

In our experience, around eight times out of ten the tenant will ask for a pet. It’s a common thing that happens throughout a tenancy.

PETS

At the start of a tenancy when being advertised, we always ask owners to consider listing a property as ‘pets upon application’ (this does not mean pets are a definite ‘yes’, it means that each application will be considered on its merits and each pet considered). Ultimately it is the owner’s decision on whether to allow pets. The benefits of allowing pets is that it will open up your property to a much larger potential tenant pool, possibly decreasing vacancy time. The reality is the most pets and pet owners are not an issue, however, not all pets are created equal! Having a ‘pets on application’ approach coupled with a signed agreement from the tenant is a good step in providing the right to ‘veto’ any pets you do not consider appropriate and safeguarding your investment.

Over 85% of our properties are pet friendly, meaning we have more tenants looking at our properties and we have less vacancy.

According to Domain, owners who considered pets can also boost their rent returns by up to 30%!

In a nation where pets are family, great tenants with a pet can be worth their weight in gold. They tend to pay rent on time, look after the property really well and they stay for 2 to 3 years!

For a Budget that made housing one of its central focuses, the federal government has three big ‘misses’ in the plans laid out on Tuesday night. Our Budget analysis considers what could be done more efficiently in the approach to Commonwealth Rental Assistance (CRA), construction, and use of existing supply.

What did the Budget get right on housing?

Increases in housing and rental costs since the pandemic have been especially hard on low income households. The decline of social housing over time has worn down the buffer between the private rental market and insecure housing, so when rents are rising as strongly as they are now, vacancies are low and demand is high, it’s low income renters who are increasingly vulnerable.

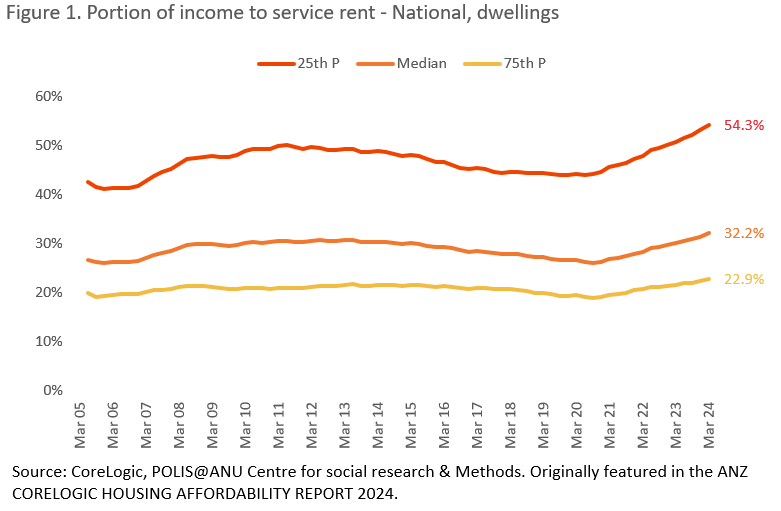

Research from the latest ANZ – CoreLogic Housing Affordability report also showed the low-income end of the spectrum saw the biggest increase in the rent to income ratio in the past four years. In March 2024, the 25th percentile rent value nationally represented 54.3% of the 25th percentile gross household income estimate (figure 1).

The Australian Institute of Health and Welfare continued to report increases in unmet requests for specialist homelessness services, which rose to 108,000 in 2022-23, most commonly because there was no accommodation available at the time.

The federal Budget has allocated funding to where it is urgently needed: crisis accommodation, social and affordable housing funding, and a boost to rental assistance for renters receiving other social assistance payments. Housing initiatives in the budget included:

An additional $423.1 million for the National Housing and Homelessness Agreement (taking total funding to $9.3 billion over five years) to deliver public housing and homelessness strategies. This also includes a doubling in funding for homelessness services at $400 million per year to be matched by the states and territories.

A second-consecutive increase to Commonwealth Rental Assistance (CRA). This $1.9 billion investment over five years will increase the maximum rate of CRA by a further 10%, following a 15% increase last year.

Additional concessional financing of up to $1.9 billion for community housing providers and other charities to support the delivery of new homes.

An additional $1 billion targeted toward crisis and transitional accommodation for women and children fleeing domestic violence, and youth.

An additional $1 billion for the states and territories to help speed up construction on infrastructure to support new housing (i.e., sewers, roads, energy and water infrastructure).

Around $90 million for training and education to boost the construction workforce.

A better targeted migration program, with student visa grants tied to the delivery of purpose-built accommodation.

What did the budget miss?

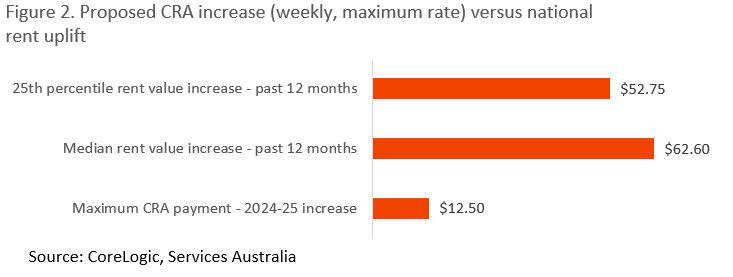

1. Commonwealth Rental Assistance was increased, but not better targeted.

The budget misses an opportunity to optimise CRA payments by ensuring they are well targeted. The productivity commission noted that in 2019-20 (albeit before rent values boomed) that 28% of CRA recipients would still have avoided housing stress without the payment, and 27% of recipients were in the top 60% of household incomes.

Figure 2 shows the maximum proposed 2024-25 increase to weekly CRA, against actual rent increases at the median and 25th percentile rent value across Australia in the year to April 2024.

A broad-based boost to CRA for those already receiving it is a pretty efficient way to ensure those in more vulnerable positions in the private rental sector can remain a little more competitive in the private rental market. But optimising the payment means more funding could be allocated to those who really need it.

2. A (bigger) boost to construction capacity.

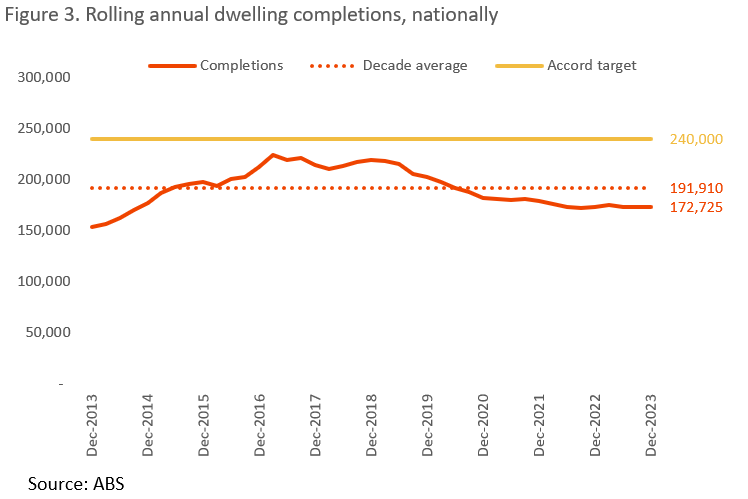

Australia’s construction sector is overheated, with too many projects stuck in the pipeline, and not enough feasibly-priced labour and materials to deliver them. The Cordell Construction Cost Index shows new house build costs are up 27.6% since the pandemic through to March 2024, and the new dwelling purchase component of CPI is up 36.1% in the same period. Our construction sector is so woefully stretched, we are unable to deliver homes at historic average volumes, let alone a stretch target of 1.2 million homes in a five-year period (figure 3).

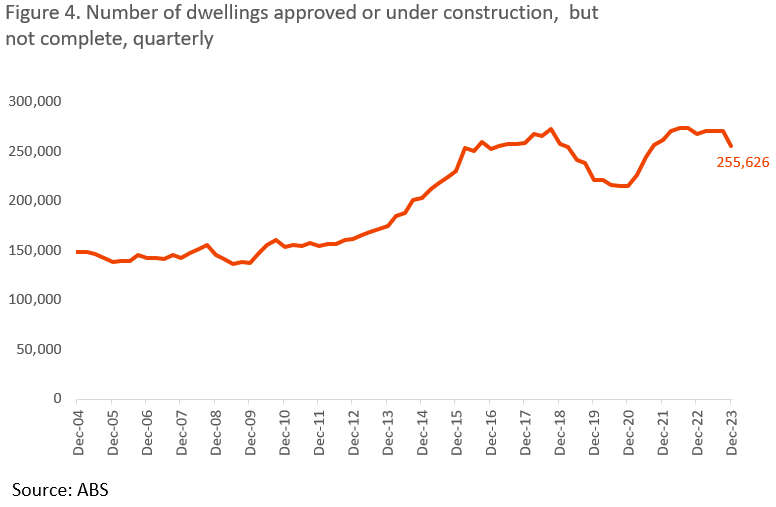

Project delays across both private and government-led housing projects are leading to a pile-up of potential supply in the pipeline (figure 4). The number of dwellings approved but not yet completed was 260,000 at the end of last year, which is actually higher than the annual accord target.

While lining up new projects to boost supply is well meaning, federal and state governments might be better off letting approvals continue to unwind in the short term amid high interest rates, so that cost pressures start to ease and the construction industry can focus on delivering the pipeline. This already seems to be working, with ABS producer price indexes now showing a reduction in the cost of steel inputs for residential construction, and the new homes component of CPI slowing to 1.1% growth in the March quarter, down from 5.7% in the March 2022 quarter. In the meantime, governments should focus on boosting the productive capacity of the construction workforce.

One way to reduce cost pressures is to beef up the construction workforce. The budget outlined around $91 million in training to do this, including:

$62.4 million for 15,000 fee-free training places at TAFE and VET vocational colleges,

$26.4 million for 5,000 pre-apprenticeship places, and

$1.8 million to fast-track skills assessment for 1,900 migrants

This could add to labour supply to the tune of 22,000 workers, representing 1.7% growth in an industry where employment had an average quarterly increase of 0.7% over the past decade. But it is not clear when the additional workers would be added, with those just embarking on the start of training certificates and apprenticeships potentially taking years to become fully qualified.

A quicker way to boost productive capacity could be to focus more on already qualified migrant labour. Reduced levies for businesses to take on overseas migrant workers, and streamlining skills recognition are important structural reforms that need to be made across a range of sectors, but especially construction at the moment. Increasing female participation in construction is a focus of this budget (noting the announcement of the Building Women’s Careers program), where women currently make up an alarmingly low 14% of total construction employment in Australia.

Aside from labour, investing in research and innovation in construction processes would also help to boost productivity. Investment that helps to scale modular builds, and embracing technologies that can further streamline design processes are some examples.

3. Demand.

Aside from a more targeted, sustainable level of migration, this Budget missed an opportunity to shape housing demand. Bold tax reform on housing has the potential to increase government revenue, and shape housing demand so that our existing housing stock is used more fairly and efficiently, at a time when new supply is challenging to deliver.

In some ways, demand for existing housing stock is increasingly inefficient among some cohorts. In previous analysis we have noted that the portion of two-person family households in dwellings with four or more bedrooms was rising over time. Working with state and territory governments to introduce land tax as a replacement for stamp duty, or factoring in the family home as an asset in the aged pension test, are examples of policies that can shape the amount of housing demanded. ANZ Chief Economist Richard Yetsenga has also pointed to inefficiencies in a supply-led housing strategy, pointing out that with 11 million dwellings for 26 million people, we should also address the issue of misallocation of existing stock rather than overstating a genuine housing shortage.

This does not have to mean upsetting rental supply by scrapping negative gearing overnight. But there is room to modify the way we tax assets like housing. Chief economist at Westpac, Luci Ellis, suggested a redesign of capital gains tax, which could be constantly discounted by the long-term inflation target to reduce market distortion. While Ellis did not specify this being applied to housing, replacing the generous 50% discount on housing investments after one year could reduce short term resales of investment property that are prompted by short term capital gain windfalls, increasing stability of tenure for renters.

Like many before it, this Budget misses an opportunity to make meaningful changes that could make a fairer and more efficient housing system in the long term.

Latest Five Star Landlord & Vendor Rate My Agent Reviews ***** Excellent Service *****

*****5 Stars*****

Excellent all round

I have used LJ Gilland Real Estate for well over a decade managing my rental property. In that time they have earned my respect as a trustable, honest and forthright team. It was an easy decision to turn to Linda and Carlos to sell my property. Their approach was devoid of the jargon and spin other real estate agents deal in. The outcome was great for both myself and the new owner. A quick sale for a good price. I highly recommend the LJ Gilland team.

Review submitted by Jason Pont (Vendor) on 30 Jan 2024

Listed on Thursday, Open House Saturday, sold on Tuesday — need we say more!!! We would like to express our heartfelt appreciation for the exceptional service provided by Carlos and Linda from LJ Gilland Real Estate during the recent sale of our property. Your professionalism, dedication and expertise truly made a significant difference in our home selling experience. From the very beginning, you demonstrated an in depth understanding of the local property market and this proved invaluable in securing the sale of our property. Throughout the process, your communication and responsiveness were exemplary and your patience in answering all our questions demonstrated your commitment to ensuring a successful sale. Your negotiation skills were impressive, as was your attention to detail particularly in organising some minor maintenance tasks that needed to be completed prior to settlement. In a competitive Real Estate market your friendly and approachable demeanour made working with you a pleasure. We wholeheartedly recommend your Real Estate services to anyone looking to buy, sell or rent. Thank you again Carlos, Linda and all of the staff at LJ Gilland Real Estate. Kind regards Wayne and Sandra Warren Review submitted by Sandra & Wayne Warren (Vendor) on 25 Oct 2023

RE BODY CORPORATE PET LAWS CHANGES FROM 01-05-2024 – Request for animals

The Regulation Amendment introduces a timeframe of 21 days (the ‘prescribed period’) for a body corporate to consider a pet request.

Deemed approvals

If the committee does not make a decision within the prescribed period, the animal is taken to be approved.

Alternatively, if a general meeting is needed to decide the request, the animal will be taken to be approved by the body corporate if either:

<![if !supportLists]>· <![endif]>a general meeting is not called within 21 days after the request is made (the ‘relevant period’)

<![if !supportLists]>· <![endif]>the body corporate does not decide the request within 6 weeks after the general meeting notice is sent out (the ‘prescribed period’).

Latest Five Star Landlord & Vendor Rate My Agent Reviews ***** Excellent Service *****

*****5 Stars*****

Excellent all round

I have used LJ Gilland Real Estate for well over a decade managing my rental property. In that time they have earned my respect as a trustable, honest and forthright team. It was an easy decision to turn to Linda and Carlos to sell my property. Their approach was devoid of the jargon and spin other real estate agents deal in. The outcome was great for both myself and the new owner. A quick sale for a good price. I highly recommend the LJ Gilland team.

Review submitted by Jason Pont (Vendor) on 30 Jan 2024

Listed on Thursday, Open House Saturday, sold on Tuesday — need we say more!!! We would like to express our heartfelt appreciation for the exceptional service provided by Carlos and Linda from LJ Gilland Real Estate during the recent sale of our property. Your professionalism, dedication and expertise truly made a significant difference in our home selling experience. From the very beginning, you demonstrated an in depth understanding of the local property market and this proved invaluable in securing the sale of our property. Throughout the process, your communication and responsiveness were exemplary and your patience in answering all our questions demonstrated your commitment to ensuring a successful sale. Your negotiation skills were impressive, as was your attention to detail particularly in organising some minor maintenance tasks that needed to be completed prior to settlement. In a competitive Real Estate market your friendly and approachable demeanour made working with you a pleasure. We wholeheartedly recommend your Real Estate services to anyone looking to buy, sell or rent. Thank you again Carlos, Linda and all of the staff at LJ Gilland Real Estate. Kind regards Wayne and Sandra Warren Review submitted by Sandra & Wayne Warren (Vendor) on 25 Oct 2023

Post a review to our Google Business profile as this is another portal for which we help spread the word and promote rental and sale listings to help our Clients i.e. https://g.page/ljgrealestate/review?gm

The information in this message is intended for the recipient named on this email. If you are not that recipient, please do not read, copy, distribute or act upon the message as the information it contains may be privileged and confidential. If you have received this message in error, please notify us immediately by return email. Thank you for your co-operation P Please consider the environment before printing this email

Posted inLJ Gilland Real Estate Pty Ltd|Comments Off on MUM CARLOS PAULA: Industry update – Pet laws and Body Corporate changes from 1st May 2024.

The Bill aims to strengthen Queensland’s residential tenancy laws. Proposed rental reforms include:

better rent protections – banning all forms of rent bidding and limiting rent increases to 12-months, attached to the property instead of the tenancy

fairer fees and charges – offering tenants a fee-free option to pay rent, ensuring any financial benefits received by rental property owners/managers are disclosed, capping re-letting costs and defining a timeframe that a tenant must receive utility bills within

making it easier for renters to modify and personalise their home

protecting renter’s privacy – extending entry notice periods from 24 to 48 hours, limiting frequent entry to a property at the end of a tenancy, offering a choice about how rental applications are submitted, creation of a prescribed application form, limiting the personal information that can be requested and collected

improving the rental bond process – any claim on a bond will be required to be supported by evidence, a portable bond scheme will be established, maximum bond requested will be no more than four weeks rent

code of conduct – a Rental Sector Code of Conduct will be developed

other improvements – improved domestic and family violence protections, greater clarity about how to end a short tenancy, improvements for rooming accommodation, ensuring a community title scheme termination is effective and allowing for better RTA operational improvements

The Bill has been referred to the Housing, Big Build and Manufacturing Committee for detailed consideration. Queenslanders are encouraged to follow the discussion on this topic and have their say on the proposed changes through the Committee process.

Latest Five Star Landlord & Vendor Rate My Agent Reviews ***** Excellent Service *****

*****5 Stars*****

Excellent all round

I have used LJ Gilland Real Estate for well over a decade managing my rental property. In that time they have earned my respect as a trustable, honest and forthright team. It was an easy decision to turn to Linda and Carlos to sell my property. Their approach was devoid of the jargon and spin other real estate agents deal in. The outcome was great for both myself and the new owner. A quick sale for a good price. I highly recommend the LJ Gilland team.

Review submitted by Jason Pont (Vendor) on 30 Jan 2024

Listed on Thursday, Open House Saturday, sold on Tuesday — need we say more!!! We would like to express our heartfelt appreciation for the exceptional service provided by Carlos and Linda from LJ Gilland Real Estate during the recent sale of our property. Your professionalism, dedication and expertise truly made a significant difference in our home selling experience. From the very beginning, you demonstrated an in depth understanding of the local property market and this proved invaluable in securing the sale of our property. Throughout the process, your communication and responsiveness were exemplary and your patience in answering all our questions demonstrated your commitment to ensuring a successful sale. Your negotiation skills were impressive, as was your attention to detail particularly in organising some minor maintenance tasks that needed to be completed prior to settlement. In a competitive Real Estate market your friendly and approachable demeanour made working with you a pleasure. We wholeheartedly recommend your Real Estate services to anyone looking to buy, sell or rent. Thank you again Carlos, Linda and all of the staff at LJ Gilland Real Estate. Kind regards Wayne and Sandra Warren Review submitted by Sandra & Wayne Warren (Vendor) on 25 Oct 2023

The decision to keep the cash rate on hold at 4.35% came as no surprise, with most economists agreeing the next move on rates will be down, although the timing of an RBA rate cut remains uncertain and dependent on inflation outcomes.

A boost to confidence: Nonetheless, the hold decision, alongside lower inflation and a growing expectation that interest rates will reduce later this year, should help to provide a further lift in confidence.

Historically we have seen a close relationship between consumer sentiment and the volume of home sales. Following the 6.2% rise in the February consumer sentiment reading from Westpac and the Melbourne Institute, a further lift in confidence could be accompanied by a rise in home purchasing. This could add to housing demand that has already remained quite resilient despite the higher interest rate environment and cost of living pressures.

Higher services inflation remains a focus for the RBA. The RBA has consistently highlighted the challenges involved with returning inflation to the target range of 2-3%. Headline inflation has reduced at a faster than forecast pace, falling from a peak of 7.8% at the end of 2022 to 4.1% annually, while the latest quarterly inflation reading, at 0.6%, is the lowest since March 2020.

However, beneath the headline result, it is clear that services inflation remains stubbornly high, reflecting tight labour market conditions but also ongoing growth in services costs such as insurance & financial services (+8.1% annual) and housing costs including rents (+7.3% annual), new builds (+5.1% annual) and utilities (+8.4% annual).

The RBA expects services inflation to decline only gradually, making the timing for a rate cut highly uncertain and dependent on further progress in reducing inflation emanating from the services sector.

Housing values continue to rise. Despite the high interest rate environment, housing values have remained broadly resilient, if not strong in some cities and regions. Upwards pressure on housing values has been supported by an imbalance between supply and demand, a situation that looks entrenched as barriers to new housing supply remain high.

Nationally, we have seen a reacceleration in the pace of value growth through the first two months of the year, which could reflect renewed optimism amid a peak in the rate hiking cycle and progress towards the inflation target.

Latest Five Star Landlord & Vendor Rate My Agent Reviews ***** Excellent Service *****

*****5 Stars*****

Excellent all round

I have used LJ Gilland Real Estate for well over a decade managing my rental property. In that time they have earned my respect as a trustable, honest and forthright team. It was an easy decision to turn to Linda and Carlos to sell my property. Their approach was devoid of the jargon and spin other real estate agents deal in. The outcome was great for both myself and the new owner. A quick sale for a good price. I highly recommend the LJ Gilland team.

Review submitted by Jason Pont (Vendor) on 30 Jan 2024

Listed on Thursday, Open House Saturday, sold on Tuesday — need we say more!!! We would like to express our heartfelt appreciation for the exceptional service provided by Carlos and Linda from LJ Gilland Real Estate during the recent sale of our property. Your professionalism, dedication and expertise truly made a significant difference in our home selling experience. From the very beginning, you demonstrated an in depth understanding of the local property market and this proved invaluable in securing the sale of our property. Throughout the process, your communication and responsiveness were exemplary and your patience in answering all our questions demonstrated your commitment to ensuring a successful sale. Your negotiation skills were impressive, as was your attention to detail particularly in organising some minor maintenance tasks that needed to be completed prior to settlement. In a competitive Real Estate market your friendly and approachable demeanour made working with you a pleasure. We wholeheartedly recommend your Real Estate services to anyone looking to buy, sell or rent. Thank you again Carlos, Linda and all of the staff at LJ Gilland Real Estate. Kind regards Wayne and Sandra Warren Review submitted by Sandra & Wayne Warren (Vendor) on 25 Oct 2023

Post a review to our Google Business profile as this is another portal for which we help spread the word and promote rental and sale listings to help our Clients i.e. https://g.page/ljgrealestate/review?gm

The information in this message is intended for the recipient named on this email. If you are not that recipient, please do not read, copy, distribute or act upon the message as the information it contains may be privileged and confidential. If you have received this message in error, please notify us immediately by return email. Thank you for your co-operation P Please consider the environment before printing this email

The 20 basis point acceleration from the 0.4% increase seen in January was the strongest monthly gain since October last year. Each of the capital cities and rest-of-state regions recorded a lift in values over the month, except Hobart where the market fell -0.3%.

“Housing values have been more than resilient in the face of high interest rates and cost of living pressures,” CoreLogic’s research director, Tim Lawless, said. “The ongoing rise in housing values reflects a persistent imbalance between supply and demand which varies in magnitude across our cities and regions.”

https://e.infogram.com/176f06eb-ec31-4ec0-83c5-6b88e7e4dc8e?src=embedPerth continues to stand out with a substantially higher rate of growth compared to any other region, up 1.8% over the month. Adelaide (+1.1%), Brisbane (+0.9%) and the regional areas of SA (+1.1%), WA and Queensland (both +1.0%) also show a consistently high rate of capital growth month-to-month.

“These regions are generally benefiting from a combination of comparatively lower housing prices and positive demographic factors that continue to support housing demand,” Mr Lawless said.

Although growth rates in Sydney and Melbourne home values have leveled out, the monthly trend has accelerated, with Melbourne emerging from a three-month slump of negative monthly movements to record a subtle 0.1% rise in February. Similarly, Sydney dwelling values have moved back into positive territory over the past two months after recording a subtle decline in November and December.

“Potentially we are seeing some early signs of a boost to housing confidence as inflation eases and expectations for a rate cut, or cuts, later this year firm up,” Mr Lawless said.

The re-acceleration in value growth has been accompanied by a bounce back in auction clearance rates, which averaged in the high 60% range through February. Consumer sentiment also recorded a solid rise in February, signaling a lift in confidence.

“Auction results and sentiment have both shown a historically strong relationship with housing trends,” Mr Lawless said. “The rise in clearance rates from the mid 50% range late last year to the high 60% range in February points to a better fit between buyer and seller pricing expectations. A rise in sentiment suggests households will have a better ability to make decisions around large financial commitments, like a property purchase.”

Although the pace of gains has shown some uplift, most regions are still recording value growth well below the highs of last year when the national index rose 1.3% in May.

“Last years’ rate hikes clearly dented capital gains, but higher interest rates haven’t been enough to extinguish growth entirely,” Mr Lawless said. “The shortfall of housing supply relative to housing demand is continuing to place upwards pressure on home values across most regions.

“However, it’s hard to see a significant rebound in values shaping up given downside factors. Affordability constraints, rising unemployment, a slowdown in the rate of household savings and a cautious lending environment, are all factors likely to keep a lid on value growth over the near term.”

Latest Five Star Landlord & Vendor Rate My Agent Reviews ***** Excellent Service *****

*****5 Stars*****

Excellent all round

I have used LJ Gilland Real Estate for well over a decade managing my rental property. In that time they have earned my respect as a trustable, honest and forthright team. It was an easy decision to turn to Linda and Carlos to sell my property. Their approach was devoid of the jargon and spin other real estate agents deal in. The outcome was great for both myself and the new owner. A quick sale for a good price. I highly recommend the LJ Gilland team.

Review submitted by Jason Pont (Vendor) on 30 Jan 2024

Listed on Thursday, Open House Saturday, sold on Tuesday — need we say more!!! We would like to express our heartfelt appreciation for the exceptional service provided by Carlos and Linda from LJ Gilland Real Estate during the recent sale of our property. Your professionalism, dedication and expertise truly made a significant difference in our home selling experience. From the very beginning, you demonstrated an in depth understanding of the local property market and this proved invaluable in securing the sale of our property. Throughout the process, your communication and responsiveness were exemplary and your patience in answering all our questions demonstrated your commitment to ensuring a successful sale. Your negotiation skills were impressive, as was your attention to detail particularly in organising some minor maintenance tasks that needed to be completed prior to settlement. In a competitive Real Estate market your friendly and approachable demeanour made working with you a pleasure. We wholeheartedly recommend your Real Estate services to anyone looking to buy, sell or rent. Thank you again Carlos, Linda and all of the staff at LJ Gilland Real Estate. Kind regards Wayne and Sandra Warren Review submitted by Sandra & Wayne Warren (Vendor) on 25 Oct 2023

Post a review to our Google Business profile as this is another portal for which we help spread the word and promote rental and sale listings to help our Clients i.e. https://g.page/ljgrealestate/review?gm

The information in this message is intended for the recipient named on this email. If you are not that recipient, please do not read, copy, distribute or act upon the message as the information it contains may be privileged and confidential. If you have received this message in error, please notify us immediately by return email. Thank you for your co-operation P Please consider the environment before printing this email

I have used LJ Gilland Real Estate for well over a decade managing my rental property. In that time they have earned my respect as a trustable, honest and forthright team. It was an easy decision to turn to Linda and Carlos to sell my property. Their approach was devoid of the jargon and spin other real estate agents deal in. The outcome was great for both myself and the new owner. A quick sale for a good price. I highly recommend the LJ Gilland team.

Review submitted by Jason Pont (Vendor) on 30 Jan 2024

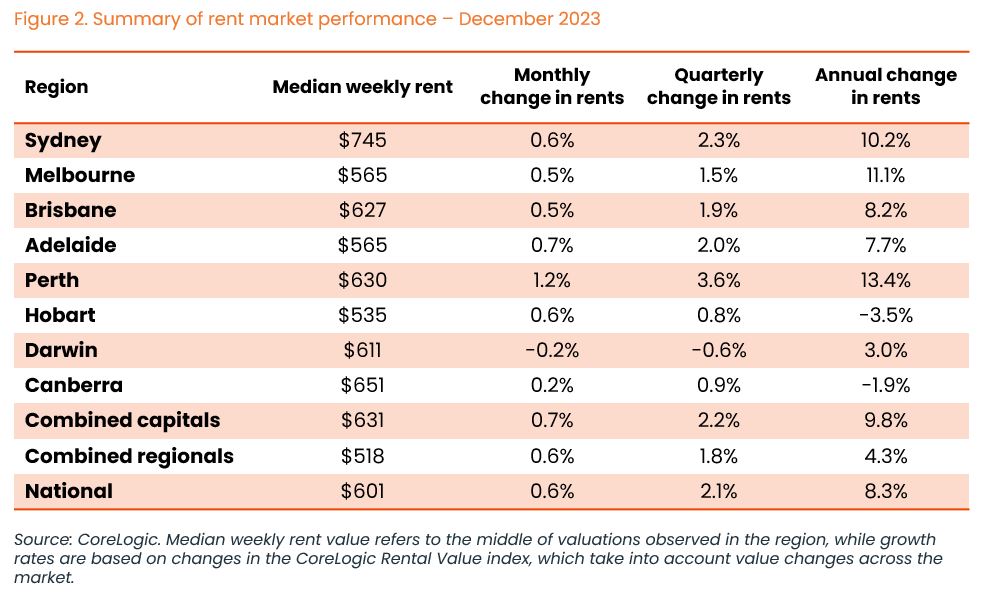

CoreLogic’s national median rent value ticked up to $601 per week last month, equating to median annual rent of $31,252 a year.

CoreLogic median rent is based on a current estimate of rent income, describing what the median dwelling in Australia would rent for if you put it on the market at any given time. The $601 median is a series high, and coincides with total annual rent increases of 8.3% nationally.

The median has increased markedly from $437 per week in August 2020, pushing annual rent values up by more than $8,000 in that time.

Recent growth in rent values, which averaged 9.1% a year for the past three calendar years, stands in stark contrast to the average annual growth rate of 2.0% in the 2010s. Since the onset of the pandemic several factors have contributed to unusually large rent rises, including:

A notable decline in the average household size from late 2020, partly driven by a reduction in share housing – meaning more dwellings were needed even when population growth was close to zero in 2021.

A rapid increase in the Australian population from late-2022 as international border restrictions were lifted.

A temporary shock to investment housing activity between May 2022 and February 2023 as interest rates rose. Investor activity has picked up markedly since, but there is still a lot of catch up required in establishing new rentals.

Longer term factors have also increased demand for rentals.

The reduction in social housing supply as a portion of all dwellings over the decades has placed more pressure on the private rental market, as has a declining rate of home ownership. Average household size has also been gradually declining over decades due to economic and demographic factors (for example, more people living alone), requiring more dwellings to house a given population.

Rent value increases have broadly outpaced wage and income rises at the national level, meaning rental affordability has also deteriorated. The portion of gross median household income required to service median rent rose from 26.7% of income in March 2020 to 31.0% in September last year. While a far higher portion of median income is required to service a new mortgage, renters tend to be on lower incomes. The latest data from the ABS suggests median gross household income was 41.8% lower across renting households than owner occupiers with a mortgage.

Median rents across the capital city markets ranged from $745 per week in Sydney, to $535 per week in Hobart. Canberra and Hobart were the only markets to see a decline in rent values through 2023, at -1.9% and -3.5% respectively.

Of 88 SA4 dwelling markets analysed (see Figure 3 on page 3), only 16 were down from historic highs. This ranged from the New England and North West market of regional NSW, which has fallen marginally from a peak in the previous month, to the Outback North of WA, where values are still 25.6% below the peak achieved amid the 2010s resources boom. Despite being well below its historic peak, the Outback North of WA had a relatively strong uplift in rent values over the past year, at 11.1%.

Across the SA4 rental markets, the highest median weekly rent was in Sydney’s Northern Beaches ($1,167 per week), followed by the Eastern Suburbs ($1,046). The lowest median weekly rent across the capital city SA4 markets was the Melbourne – West market.

Rent growth is starting to slow…

While annual growth in rents is higher than historic averages, it has broadly slowed. In 2023, rent values rose 8.3%, down from a peak of 9.6% in the year to September 2022. The slowdown has been most evident across regional Australia, where rents rose 4.3% last year, down from a 13.4% in the year to August 2021. The slowdown in capital city rent growth began more recently, easing from a peak of 10.6% in the 12 months to April 2023, to 9.8% by the end of the year (figure 4).https://e.infogram.com/cd3b303d-3231-430b-87f6-4546b0afee95?src=embed

As noted in previous research, growth in the CoreLogic rent value index tends to be a leading indicator of CPI rents. This is because CoreLogic rent measures are derived from advertised rents, where CPI measures rents actually paid by households. Rents paid tend to be ‘sticker’ than values, due to periodic leases (usually 12 months). Figure 5 shows the rolling annual change in capital city rent values versus the CPI rent measure. Historically the lag between CoreLogic and CPI rent measures has averaged six quarters, but already the monthly CPI rent indicator has shown a decline from 7.6% in September, to 7.1% at the end of November.

The slowdown in rent growth may be attributed to affordability constraints driving renters back to share housing, or to cheaper markets. Additionally, the recent resurgence in investor activity through 2023 may be gradually helping to ease supply-side constraints.

… but increases are speeding up again in capital city house markets

The easing in rent growth is good news with regard to inflation, but there was a slight pick-up in annual growth once again in the final quarter of 2023. This ‘re-acceleration’ in rents was most consistent across the capital city house markets, but was also evident in regional rent markets.

As noted in previous quarters, part of the explanation for an uptick in house rent growth may be in part due to households re-grouping into share houses. Additionally, the premium of house rents over units has narrowed in the past two years, from $63 per week at the median level to $38. This ‘catch up’ in unit rents could be making them less appealing, diverting tenants back to houses.

Part of the explanation could also be compositional: more affordable rental markets, such as regional or outer-suburban markets, are typically higher in detached houses. For example, some of the largest increases in annual rent growth towards the end of 2023 were house markets in Sydney’s Outer South West and the Blue Mountains. In Perth, the North West house market saw the biggest pick-up in annual growth.

Despite the concerning reacceleration toward the end of 2023, rent growth is still expected to slow this year. The continued increase in investment lending, a normalisation in net overseas migration and the potential for a cash rate reduction could all contribute to a slowdown. However, in the short term, the burden largely remains on tenants to secure cheaper housing, whether that be by re-forming share house arrangements, or once again looking to regional or outer suburban markets for rental accommodation.

Latest Five Star Landlord & Vendor Rate My Agent Review ***** Excellent Service *****

Listed on Thursday, Open House Saturday, sold on Tuesday — need we say more!!! We would like to express our heartfelt appreciation for the exceptional service provided by Carlos and Linda from LJ Gilland Real Estate during the recent sale of our property. Your professionalism, dedication and expertise truly made a significant difference in our home selling experience. From the very beginning, you demonstrated an in depth understanding of the local property market and this proved invaluable in securing the sale of our property. Throughout the process, your communication and responsiveness were exemplary and your patience in answering all our questions demonstrated your commitment to ensuring a successful sale. Your negotiation skills were impressive, as was your attention to detail particularly in organising some minor maintenance tasks that needed to be completed prior to settlement. In a competitive Real Estate market your friendly and approachable demeanour made working with you a pleasure. We wholeheartedly recommend your Real Estate services to anyone looking to buy, sell or rent. Thank you again Carlos, Linda and all of the staff at LJ Gilland Real Estate. Kind regards Wayne and Sandra Warren

Review submitted by Sandra & Wayne Warren (Vendor) on 25 Oct 2023

Home value performance through December across the capitals. Sydney 0.2% Melbourne -0.3% Brisbane 1.0% Adelaide 1.3% Perth 1.5% Hobart -0.3% Darwin 0.7% Canberra -0.1%

The Australian residential housing market was put to the test in 2023.

Amidst the pressure of climbing interest rates, stretched affordability and a mounting ‘fixed rate cliff’, the nation’s resilience proved to be unshakeable in some markets.

Today, we released our annual Best of the Best report which spotlights the country’s top performing suburbs, including insights on what to expect from the coming year.

So where were the country’s highs and lows? Find out exclusively in Best of the Best 2023. Read more Best of the Best 2023 features a review of the property market that was, plus an exclusive preview of what lies ahead in 2024.

It also includes national, capital city and rest-of-state region data across the following metrics:

* Top 5 sales including address, price and sale date (dwellings) * Top 5 highest total value of sales (houses & units) * Top 10 most expensive/affordable suburbs (houses & units) * Top 10 largest 12-month growth/decline in values (houses & units) * Top 10 strongest 12-month growth in rents (houses & units) * Top 10 highest gross rental yields (houses & units)

CoreLogic’s national Home Value Index (HVI) rose 8.1% in 2023, a significant turnaround from the 4.9% drop seen in 2022, but well below the 24.5% surge recorded in 2021. December’s 0.4% increase saw 2023 finish with a relatively soft monthly rise in home values.

“This was the smallest gain in our national monthly HVI since values started rising in February,” said Tim Lawless, CoreLogic’s research director. “After monthly growth in home values peaked in May at 1.3%, a rate hike in June and another in November, along with persistent cost of living pressures, worsening affordability challenges, rising advertised stock levels and low consumer sentiment, have progressively taken some heat out of the market through the second half of the year.”

Despite the annual 8.1% increase, the year was punctuated by diversity, with the annual change in housing values ranging from a 15.2% surge in Perth to a -1.6% fall across regional Victoria.

One of the main trends through the year has been the widening disparity in the rate of home value growth across the capital cities.

Dwelling values have been rising at more than 1% each month on average across Perth, Adelaide and Brisbane since May, while in Melbourne and Sydney the pace of growth has slowed sharply since the June rate hike. Melbourne values declined through November and December while Sydney home values are stabilising with a monthly growth rate of just 0.2% in the final two months of the year. The smaller capital cities have been soft through most of the year, with Hobart (-0.8%) and Darwin (-0.1%) recording an annual decline in values in 2023, while the ACT recorded a rise of just 0.5%.

“Such diversity across the capital cities can be broadly attributed to factors relating to demand and supply,” Mr Lawless said. “In Perth, Adelaide and Brisbane, housing affordability challenges haven’t been as pressing relative to the larger cities, and advertised supply levels have remained persistently and substantially below average. The cities where home value growth has been lower or negative through the year are showing higher than average levels of advertised supply alongside annual home sales which ended the year below the five year average.”

Capital cities have generally recorded stronger growth conditions relative to regional areas. Across the combined capital cities index, dwelling values were up 9.3% in 2023, more than double the 4.4% rise recorded across the combined regional index.

“Stronger conditions across capital city markets is a reversal of the early COVID trend which saw regional markets experience higher demand amid strong internal migration. Regional migration trends have mostly normalised through 2023, and the significant capital gains recorded through 2020 to 2022 has meant many regional markets have become less affordable,” Mr Lawless said.

Although housing values have risen across most regions in 2023, five of the eight capitals are still recording home values below record highs. At the end of the year, Sydney values remained -2.1% below their January 2022 peak, Melbourne values were -4.1% below their March 2022 peak, ACT values are still -6.3% below record highs and Hobart values are down -11.2%. Darwin home values are -2.8% below their cyclical high in August last year, and -7.2% below the record high set back in May 2014.

Linda-Jane 琳达-简德贝洛 Debello LREA, LJ Gilland Real Estate Property Sales & Management Est 1996 07 3263 6085 | 0409 995 578 http://www.ljgrealestate.com.au linda@ljgrealestate.com.au PO Box 19, Zillmere QLD 4034

Latest Five Star Landlord & Vendor Rate My Agent Review ***** Excellent Service ***** Listed on Thursday, Open House Saturday, sold on Tuesday — need we say more!!! We would like to express our heartfelt appreciation for the exceptional service provided by Carlos and Linda from LJ Gilland Real Estate during the recent sale of our property. Your professionalism, dedication and expertise truly made a significant difference in our home selling experience. From the very beginning, you demonstrated an in depth understanding of the local property market and this proved invaluable in securing the sale of our property. Throughout the process, your communication and responsiveness were exemplary and your patience in answering all our questions demonstrated your commitment to ensuring a successful sale. Your negotiation skills were impressive, as was your attention to detail particularly in organising some minor maintenance tasks that needed to be completed prior to settlement. In a competitive Real Estate market your friendly and approachable demeanour made working with you a pleasure. We wholeheartedly recommend your Real Estate services to anyone looking to buy, sell or rent. Thank you again Carlos, Linda and all of the staff at LJ Gilland Real Estate. Kind regards Wayne and Sandra Warren Review submitted by Sandra & Wayne Warren (Vendor) on 25 Oct 2023 https://www.ratemyagent.com.au/real-estate-agency/lj-gilland-real-estate/property-listings/11-yovan-ct-loganlea-ahhh65?agentCode=cp733

The information in this message is intended for the recipient named on this email. If you are not that recipient, please do not read, copy, distribute or act upon the message as the information it contains may be privileged and confidential. If you have received this message in error, please notify us immediately by return email. Thank you for your co-operation Please consider the environment before printing this email

Best Regards.

Best Regards.

{kind=link}

You must be logged in to post a comment.